Most people still don’t know anything about Bitcoin except its price. But they don’t know why Bitcoin has a price in the first place. Hence the skepticism. When you don’t know why something has a price, it is impossible to understand how much it can really be worth.

Misir Mahmudov

In the attempt to dismiss the space as a whole, mainstream media commentators often state that cryptocurrency is 100% gambling or speculation — just a number on the screen intended to be bet on. It is important to note that people have considered Bitcoin to be grossly overvalued since as low as $0.70 per BTC. Indeed, as Misir Mahmudov succinctly points out, they do not know why Bitcoin needs to have any price > 0 at all.

What if there was a way to differentiate between use value and speculative value?

First, let’s define some terms:

Physical crypto is the digital asset itself. This is also known as “spot” or “coins.” These exist on a blockchain.

Financial crypto is the financial derivative on the physical crypto. This can be a perpetual swap or a future, and exists on centralized exchanges such as CME, Bitmex, Deribit, etc.

Let’s look at some commodities, both digital and non-digital, to clarify what we mean.

Gold

In gold, there is a concept of an EFP (exchange-for-physical) market, where one party wishes to convert physical gold to financial gold or vice versa. A natural buyer of a gold EFP (long future/short spot) might be a gold miner who had previously shorted futures to hedge his expected production and now can deliver physical gold. Conversely, a natural seller of a gold EFP (short future/long spot) might be a gold investor who had bought futures and now wants to take delivery of physical gold itself.

For a financial investor, he may prefer simply buying gold futures at the CME and rolling them (extending the maturity). Through leverage, this is capital and tax efficient, and he can invest in this future alongside many other futures (stock index, oil, etc) as well as rebalance between them as part of an overall portfolio.

For a long-term holder of gold, he may wish to own the gold itself so as to truly benefit from its safe haven properties. For instance, Lee Robinson urges gold investors to consider holding physical gold in at least three different locations around the world: Australia, Canada, and Switzerland. The idea behind this is that owning gold as safe haven but keeping it as a financial derivative at your broker or in a vault in your own country is likely to backfire exactly when you need it the most. Will the CME be around? Will the vault in your country grant you access to your gold? How do you know the gold is even there?

For the wealthy global elite, many who have survived through communist and totalitarian regimes, this is not mere theory but lived experience.

Bitcoin

The demand for physical BTC arises from its censorship-resistance and its status as the earliest and most liquid blockchain.

- physical BTC is the only accepted collateral on websites such as Bitmex. Security and liquidity are the main requirements, and

consequently they have no desire or need to add any other forms of collateral (esp fiat) - throughout BTC’s history, many airdrops and forks(digital assets which seek to credit those holding physical BTC with balances on the new blockchain) have occurred, giving those who hold physical BTC an edge

- anyone seeking to upload value from fiat to the largest and secure blockchain is a natural buyer of physical BTC

XRP

There is active demand for physical XRP from trading firms doing cross-exchange arbitrage. Having XRP collateral enables them to transfer value extremely quickly and cheaply between exchanges, thereby capturing various arbitrage opportunities faster than those using other blockchains to move value.

- fastest transactions among top coins

- lowest fees for transactions

Ether

Ether is used to pay for transaction fees on the Ethereum network and also as the native asset of various applications built on Ethereum.

- used as collateral in Maker to borrow DAI, a USD stablecoin

- used to pay fees for smart contracts

- after the switch to Proof of Stake, staked to become a validator on the network and earn rewards

The existence of non-price sensitive and non-speculative use cases are already here and can be seen in the behavior of derivative markets. Just as with gold, so with BTC, XRP, and ETH — owning physical coins gives the buyer the ability to transfer and store value digitally at varying levels of security, decentralization, and programmability. Owning financial crypto, while having the benefit of leverage and ease of access, lacks the value proposition of crypto itself.

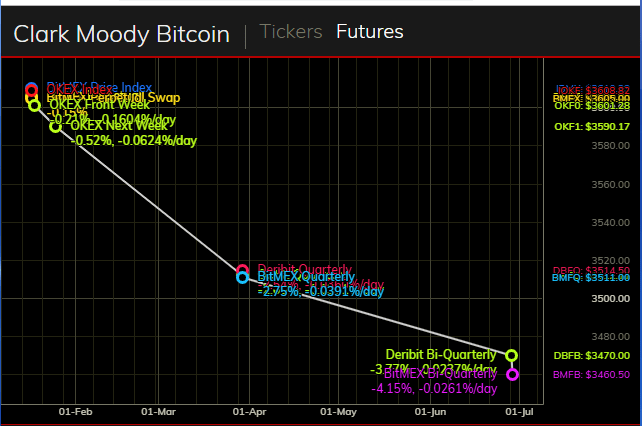

In a bull market, derivatives trade at a premium to spot because getting fast access to the price appreciation of crypto becomes more important than the properties of crypto itself. In a bear market, the interest in owning financial crypto declines while the interest in physical persists — leading to a discount to spot. From the above chart, we can see that the market demand for spot-BTC is higher than the demand to own financial BTC (around 4% for 6months).

These dynamics allude to the underlying fundamentals of crypto and should be intensely studied both by crypto-natives as well as by open-minded skeptics seeking to better understand these nascent markets.

Thanks to Hasu for his feedback.