Written by Hasu and Alexander Liegl

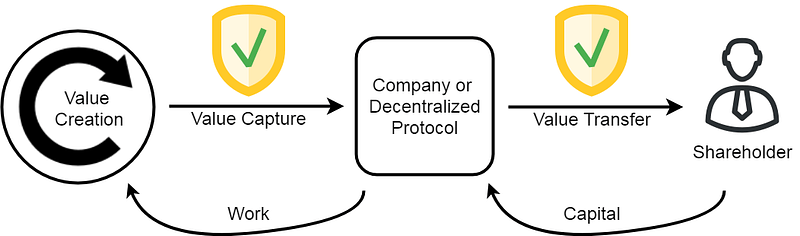

The point of this essay is to show how value flows from users to shareholders in both companies and decentralized protocols and give the reader a mental model for making sense of profit share tokens.

Premise 1

A centralized company captures some of the value it creates.

They do that by charging more for a service or product than the cost the produce it, for example Apple selling the iPhone.

Premise 2

Investors purchase equity in a company to benefit from its value capture.

As a rough simplification, when Apple is done selling iPhones for the year, they substract all of their expenses and put their money into the company bank account. Investors have a legal claim on a fraction of that bank account as well as all future money that will be deposited.

Premise 3

Decentralized protocols are disintermediating, which allows for products and services that centralized companies cannot compete with.

Eliminating the man in the middle can open new value creation that is entirely closed for centralized companies. As a result, they can

- serve illegal usecases and markets

- reduce counterparty risk (for example enabling trustless exchange of value or private information)

- eliminate rent and drive down prices

Premise 4

The flow of value from consumers to investors is defended at two important interfaces, (1) at the value capture (from revenue to company books) and (2) at the value transfer (from company books to investors).

In the following two premises, we will take a look at how the two interfaces are defended and where they are leaky.

Premise 5

Both companies and decentralized protocols defend their value capture via moats.

In absence of moats, profitability can be reached for a while but is not sustainable because other companies will start competing for the same customers, thus driving down margins into a new, lower equilibrium.

Premise 6

Companies and decentralized protocols have different moats.

Typical moats among centralized companies are…

- Economies of scale

- Government regulation

- Brand / user trust

- Intellectual property or patents

- Magnitude of network effects (and more)

Typical moats among decentralized protocols are:

- Magnitude of network effects

- Quality development team

- Organic user adoption

- Integration into financial infrastructure

The lack of IP and patents is a huge problem for investors and great news for users of decentralized protocols.

The same disintermediation that allows decentralized protocols to tap new fields of business also makes it hard to capture the value that is being created. To be disintermediating the protocol has to be open source, which means that anyone can fork it and spin up a cheaper, but otherwise perfectly equal, alternative.

Strong network effects and integration into financial infrastructure will most likely be reserved for the largest protocols. A quality development team will usually be the strongest moat that a protocol can have in early days. With the value of that team rises and falls the defendability of the rent-seeking mechanism that they created. Once network consensus turns against them, for example because the network is working fine and no more important features are required, the team can be forked out together with the rent.

Premise 7

Both companies and decentralized protocols defend their value transfer via property rights.

Property rights are the only thing that gives a stock, bond or financial contract any value. Every contract is only as valuable as its enforceability. Your equity in a regular company is guaranteed by the legal system of your jurisdiction, whose rules are respected because it can punish bad actors for misbehavior. Conceding power to an institution and making defection more costly enables more actors in a society to cooperate and to do business together.

Profit share in a decentralized protocol however cannot be secured by the same institutions. The property right cannot be guaranteed, because there is no punishment for defection. Instead of the legal system, the value transfer is defended only by the consensus of the network participants. Are they willing to pay the current rent or can they fork the protocol and reduce or even remove it?

Examples

After showing the challenges for decentralized protocols to defend their value capture and transfer, we are going to look at two examples.

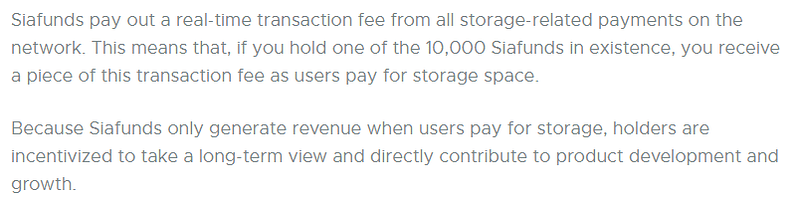

(1) Siafunds

The Siafund token is only defended by the current Sia dev team. Once the network agrees that the Sia team is no longer worth that rent that they extract from the network (for example because the network is working fine without further development), the Siafund token runs the risk of being forked out of the protocol. In centralized companies, virtually all of the valuation is from future cashflows. For a decentralized protocol like Sia, a very steep discount should be applied to that value as an ongoing enterprise. One potential solution would be to offer bonds with a shorter expiry date, thus eliminating much of the uncertainty around pricing the future.

(2) Binance/BNB token

As a more mixed counter example we want to offer the Binance token. Because it is backed by a centralized company, it doesn’t have the risk of being forked out. While roots in the physical world give more defensibility of value flow to the investor, it hinders the company from tapping into the potential for value creation that is exclusive to decentralized protocols (disintermediation and serving illegal products and markets).

The Binance token is best imagined as a second class of (pseudo-)equity that targets a different audience of buyers. It has two major use cases. The first is a discount/loyalty model for power users of their service. The second is buying back tokens, which is a more tax efficient way of paying a dividend to investors.

While the idea of offering different classes of shares that benefit different people is very good and should be explored further, these pseudo-shares require trust and are not legally enforceable. Binance could withdraw support for it at any time, for example because regular shareholders feel like the dividend that Binance pays to their token holders should go to them instead. We invite experimentation with different classes of shares once they are all equally enforceable. Futhermore, it’s not clear that Binance couldn’t have reached an equal or better outcome by using an established subscription based loyalty model like Amazon Prime.

Conclusion

In any for-profit enterprise, there are two interfaces where shareholder value is defended: at the value capture, and at the value transfer. We would expect value capture in decentralized protocols to mean-revert much faster because it’s very hard to have a meaningful competitive moat to sustain profit margin. Once profit margin gets too high, competitors will be enticed to take share by creating a cheaper competitor, or even easier, fork the protocol and lower the rent.

In summary, it’s significantly harder to benefit from value creation in decentralized protocols compared to companies as there is no legal ownership protection and few barriers to entry aside from network effects and the development team. We suggest that profit shares in decentralized companies should be valued at an extremely steep discount to their current cash flows relative to centralized entities with governance and a competitive moat.

This essay is part of a loosely connected series, starting with “A deductive valuation framework for cryptocurrencies”.

Thank you to Nic Carter, Ataraxia and Su Zhu for their feedback.