In the first article, we discussed the promise and illusion of custody. Next, we turn our attention to the proliferation of Professional Funds: crypto HFs (hedge funds) and crypto VCs (venture capital). Do these represent crypto adoption? Is the herd coming?

Professional Funds

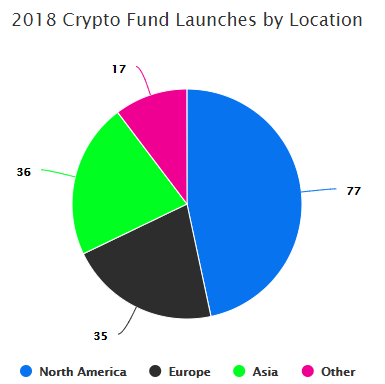

According to Crypto Fund Research, there were 198 fund launches in 2017, of which 112 were HFs and the remainder VCs. In 2018, there are projected to be 220 fund launches spread across the world. Notably, crypto funds account for one in five new launches across the entire investment fund space.

It is important to note the basic difference in strategy for HFs vs VCs. The former trades on shorter time horizons and moves in and out of positions, using capital not just for asset allocations but also for derivatives/hedges. The latter seeks to invest on higher multi-year horizons and can traditionally tolerate low levels of liquidity. I will avoid discussing market-neutral quant/arbitrage funds here as these make up a small % of the overall capital.

Prolific cross-investment between HFs and VCs has been the prevailing theme since 2017. I’ve listed below some known fund-to-fund entanglements:

a16z: to blocktower, metastable, polychain, dnausv: to multicoin, blocktower, polychain, placeholdersequoia: to polychain, metastableblocktower cio: to multicoinneural: to blocktowercraft ventures: to multicoinmetastable founder, blocktower cio, neural cio, multicoin partner, pantera partner, scalar partner, amentum partner: to protocol ventures: to metastable, neural [note the circularity]

A March 2018 round for Multicoin looks like this: “Other new investors in the fund include Chris Dixon, Compound, Vy Capital, Passport Capital, Adam Zeplain of Mark VC, Ari Paul of Blocktower and Elad Gil.” Compound itself is an ICO, so there appears to be funds investing in ICOs investing in funds.

I see five main reasons for this trend, and none of them are good.(1) Creates the perception of massive institutional buy-in / thought leadership behind any one specific idea. See below from Mainframe’s site:

(2) Enables the VCs at the top of the pyramid to claim they have never sold a crypto investment, while letting the HFs do the churning.

(3) Generates layers upon layers of fees vs LPs, as well as CEO/CIO/Co-Founder job titles for as many people as possible.

(4) Attempts to create an exclusive chain of access to maintain intellectual cohesion.

(5) Basic FOMO (Fear of Missing Out). Everyone wanted to make the easy money of flipping ICOs.

While the reasons are slightly different, the parallels to the high levels of crossholding that we saw in Japan during their asset bubble are inescapable. NLI Research estimates that “strategic shareholding ratios among Japanese companies have declined from 45.8% in fiscal 1987 to 27.1% by fiscal 2002, while crossholdings have fallen from 18.4% in 1987 to 7.4%.”

If we were to calculate strategic shareholdings for certain ICOs (we cannot as the token data is not publicly available, unlike for equities), this would likely be well in excess of the 45% high at the top of the Japanese bubble. Importantly similar in both cases is the concept of anti-competitive collectivism: the idea that a group of people band together to promote a fledgling industry and evangelize its tenets.

Although some may construe this as noble, I would posit that this has led to an enormous amount of herding and mal-investment. In traditional finance, funds compete with each other for deals, investments, and talent. HFT firms do not typically take friendly stakes in one another. Neither do traditional hedge funds, VCs, or private equity firms. It is also highly unusual for GPs to invest into other funds via their main fund itself, and reveals a lack of coherent internal thesis.

Many of these crypto fund managers had their chief credential being their relatively early buy-in into cryptocurrencies as a whole. In part this informs why much of 2017/2018 has been about “finding the next Ethereum” as opposed to questioning whether such a finding is possible. As Brett Winton notes, many of them have never seen a proper financial cycle. Even late in this particular cycle, the level of due diligence is still not at the level that we see in other financial industries. For instance, Set Protocol estimates that only 30–40% of their own investors read their whitepaper.

It is obvious why these funds have been able to attract LPs. The idea of being able to monetize access and club deals is seductive to high-net-worth individuals and family offices who view these funds as a way to allocate to experts and “get in on the action.” It absolves them of the need to think on their own about what crypto actually is and how it should fit within their portfolio.

Fortunately, the market has begun to punish these poor choices and likely will continue to do so. LPs backing funds to access club deals is not crypto adoption, and neither is the same 5 funds reinvesting in each other using different names. Not only is it antithetical to the concept of crypto as a decentralized & open ecosystem, it’s a shaky foundation for any industry.

Hopefully as the industry matures, LPs will begin asking difficult questions to their GPs and reward the ones who can clearly articulate a multi-year vision. Some may redeem to buy crypto itself and unlock the benefits of self-custody. We will see healthier valuations, fewer funds backing each round, more unique ideas getting funded, and competition rather than collusion.Delivering adoption and long-lasting value will be seen as the metric of success, not raising a 9 figure token sale or fund.