Representatives of BitMEX, the largest Bitcoin exchange, love to show how much they care about the crypto community. When their charismatic CEO Arthur Hayes goes on CNBC to say nice things about Bitcoin, the recordings go viral on Twitter, and when the amazing BitMEX Research puts out a new blog post, everyone stops their day to read it.

But a series of recent issues with the exchange leads me to believe that they have a hard time acting ethically once it gets in their way of making more money. That is a problem because BitMEX is based in the Seychelles and doesn’t submit to any regulator.

BitMEX is an opaque entity that wields disproportionate influence in the industry. In an attempt to understand the machinations of the exchange, I did two things:

- Interviewed everyone who was willing to talk to me about BitMEX, listening to their most frequent and reasonable concerns.

- Built a mental model of how I believe BitMEX operates and what their incentives are.

That led me to identify three main concerns.

- “BitMEX trades against their customers”

- “BitMEX weaponizes their server problems”

- “BitMEX monetizes customer liquidations through their insurance fund”

I will explore the validity of each concern and see if they fit the BitMEX incentive structure. Last, I will propose a set of solutions that should ameliorate the concerns going forward.

This article is sourced from many in the industry, most of whom are customers of BitMEX to this day. All have chosen not to disclose their identities.

1 — “BitMEX trades against their customers”

On April 30, 2018, BitMEX released a blog post that announced an update to their Terms of Service. It says that “BitMEX has a for-profit trading business that, among other things, transacts in products traded on the BitMEX platform. The trading business primarily trades as a market maker”.

Market makers continuously quote buy and sell orders to provide liquidity on exchanges. They are the ones filling the order books with orders that others can then match. The prices quoted by market makers are typically placed below and above the last price. This way, they profit from people who pay for the privilege to have their trade executed immediately (by taking instead of making a competitive order).

Market makers post a quote to both the buy and sell side of the order book. If their sell order gets taken, they look to close out a buy order as well. This guarantees that the market maker stays as neutral as possible to the general price movements of the market. Instead of from up- or down movements of the price, he instead profits from the spread that his customers are willing to pay for the immediate liquidity he provides.

If the desk only engaged in market making, that would be fine, as it would help the users of the exchange fill orders. But all of my interviewees have challenged this statement. Here is why they are skeptical:

BitMEX hid the desk from their customers.

If the desk engaged in market making and nothing else, many wonder why BitMEX was so bent on keeping its existence a secret. When BitMEX finally came clear about it in April of 2018, it had been a persistent rumor for a long time.

BitMEX may have lost their legal counsel after announcing the desk and kept that a secret, too.

In their original blog post on April 30, BitMEX still lists the renowned international law firm Sullivan & Cromwell as their lead outside counsel.

But somewhere between May 5 and May 22, they silently removed Sullivan & Cromwell from the post.

Why did BitMEX and Sullivan & Cromwell separate? Is it possible that S&C had issues with the plans that BitMEX had with their desk? I reached out to S&C with a request for comment and will update my article when they get back to me.

The desk makes a profit from trading.

While BitMEX admits the desk is a for-profit operation, they claim that its profit doesn’t come from trading:

According to them, the desks’ goal is to be breakeven (PnL stands for profit and loss, or net income) and that the desk instead makes money from a service fee paid by the main business.

This method would guarantee that the desk sticks to market making, a positive-sum activity that benefits the exchange (which gains volume), market makers (who capture spreads), and traders (who gain liquidity). Trading for profit, on the other hand, is strictly a zero-sum game that merely provides the illusory benefits of a well-operated exchange.

Unfortunately, there is no way for the customers to verify the desk’s business model, as BitMEX has never opened up to an external audit of their business structure. Customers have to take their word for it, and most don’t believe them.

The desk is not market-neutral.

We established above that market making attempts to be market neutral and not benefit from the market moving up or down. The opposite of that would be to take a directional position, which can be short or long. If you go short, you benefit from the market moving down, and if you go long, you benefit from the market moving up. Doing this would be a prerequisite for the desk to make a profit from trading.

The desk isn’t held to the same rules as everyone else.

A BitMEX desk that is allowed to trade on their exchange freely is bad in theory but even worse in practice. Because it creates the incentives to go the extra mile and give it unfair advantages over the other customers. If the owner of an online casino was allowed to play in his own poker games, we have to ask: can he resist the urge to view everyone’s hole cards?

This brings us to the most important job of any peer-to-peer exchange: to guarantee fair competition between all customers. It comes down to two things: equal access to information, and equal priority of access.

Equal information is important because just like in a poker game, it helps to know as much as possible about the cards everyone else is holding. Some information is available to everyone, like the composition of the order book or past price developments. Other information is private, like the degree of leverage that each position uses and at what price it runs out of margin, triggering its liquidation.

Knowing the liquidation points of all other players would allow you to move the market by placing a large buy or sell order to and trigger this a so-called chain of liquidations (also known as a cascading margin call). When, for example, a lot of leveraged shorts get liquidated, they enter the market as forced buy orders, pushing the price even higher. At this point, you would sell into this “buy wall” to close your trade with a handsome profit.

Of course, BitMEX has explicitly denied granting privileged information to their trading desk. It has not commented on the second requirement, equal priority of access. This refers to the speed and reliability in communicating with the exchange and placing your orders. Access speed in trading is so important that a whole industry, called high-frequency trading or HFT, has been built on it. This led traditional exchanges to invest tons of resources to iron out even small perceived imbalances in their system, which would otherwise get exploited and make the exchange too unfair for regular customers.

While access speed is hard to measure, there is a concrete reason why people suspect BitMEX gives unfair advantages to some customers, most of all their trading desk.

2 — “BitMEX weaponizes their server problems”

BitMEX is long known for having frequent server problems, which BitMEX has historically blamed on using a very safe, but computationally expensive, trading engine.

A high level of system integrity is important because of all the leveraged positions that BitMEX has open with their customers at any time. Any small bug in the system could lead to a user being allowed to lose more than he has, which would endanger the financial stability of the entire exchange.

To prevent that, BitMEX has a risk management engine which activates on every tick. A tick is the smallest possible price movement, in the case of BitMEX’s perpetual swaps, $0.50. Once the price moves, the risk management engine will perform an entire audit of the system and de-risk it by performing the necessary liquidations.

While the risk management usually is very fast, sometimes it can bring the entire system to a halt. Then the exchange stops working, and everyone has to wait for service to return. BitMEX calls these events “server overloads”, and they now regularly happen around 2–3 times a day.

In theory, BitMEX allows open positions to be closed during server overloads with supposed priority. But in reality, it’s impossible because users either get locked out of their accounts and are unable to sign back in, or they simply can’t process any trades, including closes or cancellation of orders.

These times when users lose their ability to trade are very problematic for a couple of reasons:

Some people can trade through overload.

While regular users can’t get orders through or even access their accounts, orders will continue to get filled, and the market keeps moving. This led many users to the impression that some parties have priority access to submit their orders and are unaffected by the server problems.

Naturally, the main target of suspicion for this preferred treatment is the BitMEX trading desk, but rumors say that they also grant it to certain high-frequency trading firms. One interviewee described it as follows: “Imagine you’re in a fight, but you have your hands tied behind your back. That is how overloads work where some people can keep trading while you can’t”.

There are two major ways that you could benefit from trading through overload:

You can arbitrage during overload.

Imagine the price of Bitcoin moving up 100$ on the other exchanges while everyone on BitMEX is frozen in time. If you could trade on BitMEX, you suddenly have access to a ton of liquidity a the old price level. You can buy it on BitMEX and at the same time sell for the new price on other exchanges to benefit from the spread.

You can trigger a chain of liquidations during overload.

We mentioned these earlier as a way to benefit for traders who have inside information about when other players get liquidated. But they also come into play here, because the majority is simply unable to close their positions in time. If you wanted to exploit this as a priority user, you would move the price with large orders while others aren’t trading on BitMEX to move where you want it. This would result in stop-losses activating as well as liquidations occurring once other exchanges move towards the Bitmex price since Bitmex is the dominant exchange. These liquidations and stop-loss orders entering the market will move the price further and trigger further liquidations. This is when you sell and book a decent profit.

So far we established how the BitMEX desk or another priority user can make a profit by taking directional positions. They can either have preferred information or priority access, most visibly in times of server overloads. The frequent occurrence of this scheme and inability or unwillingness of BitMEX to fix the problems have led many to believe that MEX must be doing it on purpose. If that’s true, we can say that they weaponize server problems against their customers.

We also established that a common way to benefit from potential preferred information or access would be to chain liquidate the other, second-class customers. We will now see that BitMEX has found a second way to benefit from liquidations.

3 — “BitMEX monetizes customer liquidations through their insurance fund”

To understand how their insurance fund works, we need to take a quick step back and look at liquidations. Once a position is taken over by BitMEX for liquidation, they are looking for buyers or sellers to close that position before the margin entirely runs out. If not enough liquidity is available at the target price, BitMEX performs an exchange-wide “auto-deleveraging” (ADL), where traders with opposing positions are automatically closed out to create the necessary liquidity.

If BitMEX closes a position in time, often some change from the margin is left over. This money goes into an insurance fund. In return, the fund steps in before ADL is about to happen. Many traders told me it’s a good thing to know that ADL can never happen to them, but there are some major problems.

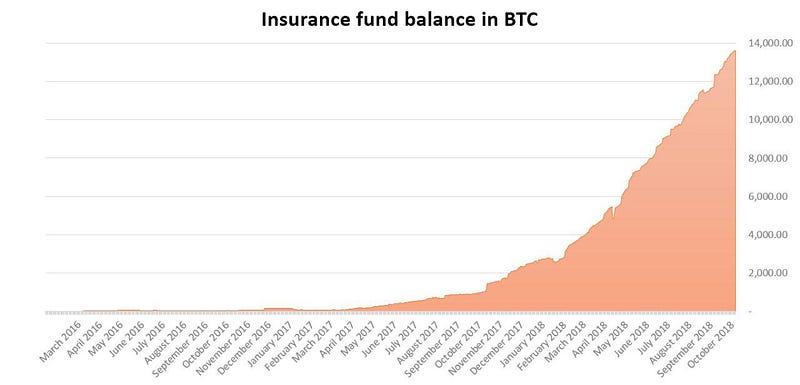

The fund has grown much larger than necessary.

Between 2016 and today, it has grown steadily to more than 14.000 Bitcoin (almost $100M at today’s prices!), 11.000 of which were added in 2018.

How do we know this kind of insurance is unnecessary? There was one day in history where the fund lost 641 Bitcoin, and three more where it lost around 100 Bitcoin. All other losses were in the lower single digits. Even by very defensive estimates, it is overcapitalized.

BitMEX views the fund as an asset on their balance sheet.

First, the money is not stored in a segregated account. Second, BitMEX doesn’t say how large they intend it to grow, or what will happen to the excess Bitcoins in it. This indicates to me that they view the fund as another asset on their balance sheet, that they can grow as much as possible and eventually liquidate.

Money disappears from the fund once a quarter.

There was a brief episode earlier this year where BitMEX claimed that a smart trader had found a way to exploit the fund using a quarterly futures contract. This lead BitMEX to partition the fund, so that every contract has their own smaller fund inside the large fund.

Most contracts on BitMEX are of the quarterly futures type, which runs for one quarter and then expires. Then BitMEX resets the partition of these contracts to zero. However, the money from the past quarterly simply disappears. It’s not carried over to the new contract, yet it’s not returned to customers or even visibly removed from the fund balance.

The fund makes BitMEX significant money from liquidations.

If it’s true that BitMEX considers the fund another asset on their balance sheet, we can consider it their second additional income stream other than commissions.

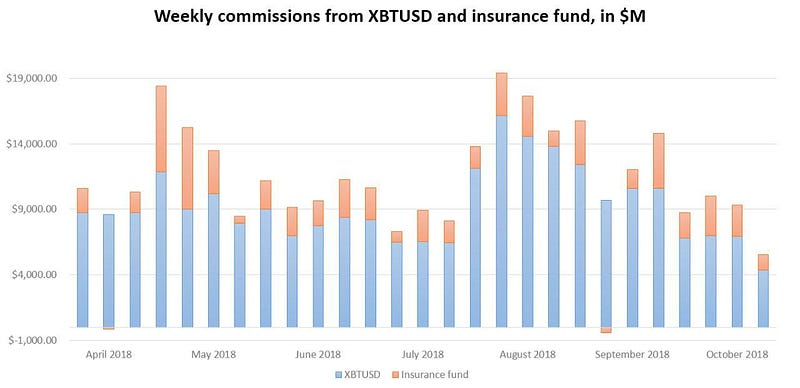

If you thought that their income from the fund is too small to matter compared to their commissions, you would be mistaken. I compared the growth of the fund to their commissions from their flagship product, the XBTUSD perpetual contract:

As you can see, the fund commissions are a significant portion of their income. During some weeks in April, the fund made 50% to 66% as much money from liquidations as BitMEX made from their most-traded contract.

The dark power of incentives

So what do I think after comparing the strongest concerns about BitMEX with their visible incentive structure? They look damn reasonable to me. I am worried that BitMEX has created two additional income streams that incentivize them to do unethical things to their customers.

- First, their desk could actively trade against their customers.

- Second, their insurance fund could be used to monetize liquidating their customers.

- Both of these income streams could be supported by giving out preferred information or access as well as by weaponizing overloads that freeze the majority of their customers and turn them into easy prey.

There is not enough evidence to conclude that BitMEX is definitely guilty of these things. But we can see that the incentives for them exist. Charlie Munger once said, “Show me the incentive and I will show you the outcome.” The same applies to BitMEX.

A list of suggestions

I don’t know if the allegations are true or not, but I would still like BitMEX to address them. For this reason, I collected a series of suggestions that would ease the mind of their customers by visibly shifting the incentives for BitMEX to maximize money from commissions again instead of from trading PNL and liquidations.

Rework the insurance fund.

- Put a hard cap on the size of the fund. It is already larger than it needs to be. If the fund is allowed to grow indefinitely, people will continue to believe that you use it as a third income stream. The cap could be dynamic based on the volume of the contract. Something like 3000 BTC for the XBTUSD should be enough.

- Be transparent about how much money is reserved for each contract, and store the money in segregated accounts. Be transparent about what happens when a contract expires.

- Stop taking money from liquidations until the fund has shrunk below the new cap. Instead, return it to the person who got liquidated.

Associate a cost with continuous overloads.

- Stop accepting new signups if your problems are really based on technical and not ethical problems.

- Compensate users who get disadvantaged by overload with temporary fee rebate.

- Consider building a colocation center where you give all clients the option to physically connect to your servers. That would eliminate the concerns that some customers secretly have more direct connections than others.

Return to the foundational idea of a peer-to-peer exchange.

- Consider closing your desk as an act of transparency, even for the purpose of market making. Instead, better incentivize outside market makers.

- Allow new products like UPs and DOWNs to be traded against other users instead of the market maker.

If BitMEX doesn’t currently benefit from trading PnL or liquidations, they have little to lose from implementing most of these changes. It would only make their business model more transparent.

To me, BitMEX is an important case study. If a company submits to regulation, that means they accept punishment if they misbehave. BitMEX does not do that. If they misbehave, there is only the free market to punish them for it. But what if the company has a quasi-monopoly like BitMEX? Or the market never even learns of the misbehavior to start? I hope that my article can serve as the start of a dialogue between BitMEX and their customers to addresses these serious concerns.

Bitmex didn’t respond to my request for comment.